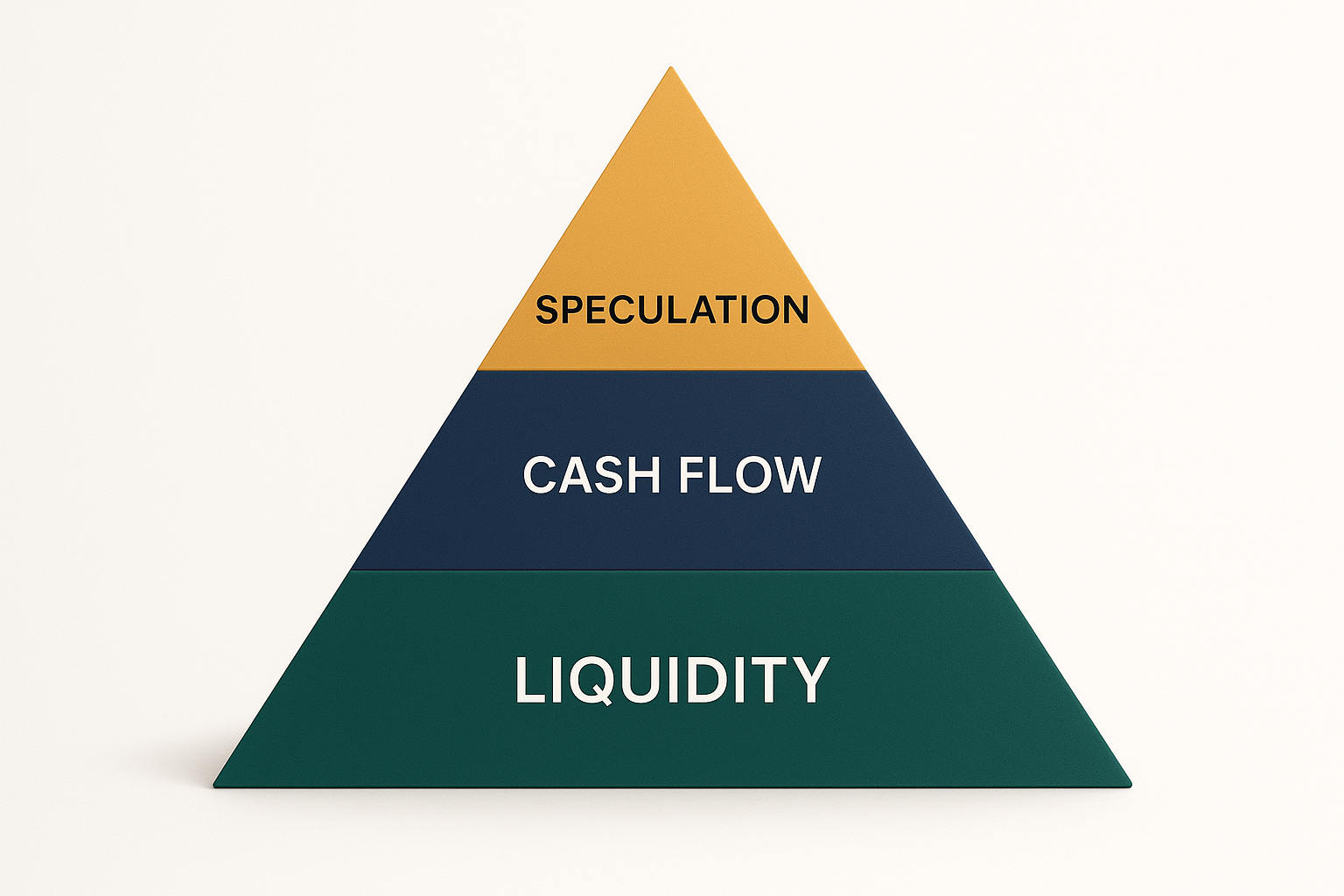

The Wealth Pyramid™

Most People Build Their Portfolio Upside Down

This strategy starts by protecting time and decision-making power with structured liquidity—then layers in income and opportunity.

Liquidity (Foundation)

Permanent life insurance provides the stable, accessible base

Cash Flow (Growth)

Income-producing assets and business investments

Speculation (Opportunity)

High-risk, high-reward investments and ventures